此部落格将停止更新,请点击以下链接阅读最新帖子:

http://gilbert-investment.blogspot.com/

2015年1月26日星期一

2015年1月17日星期六

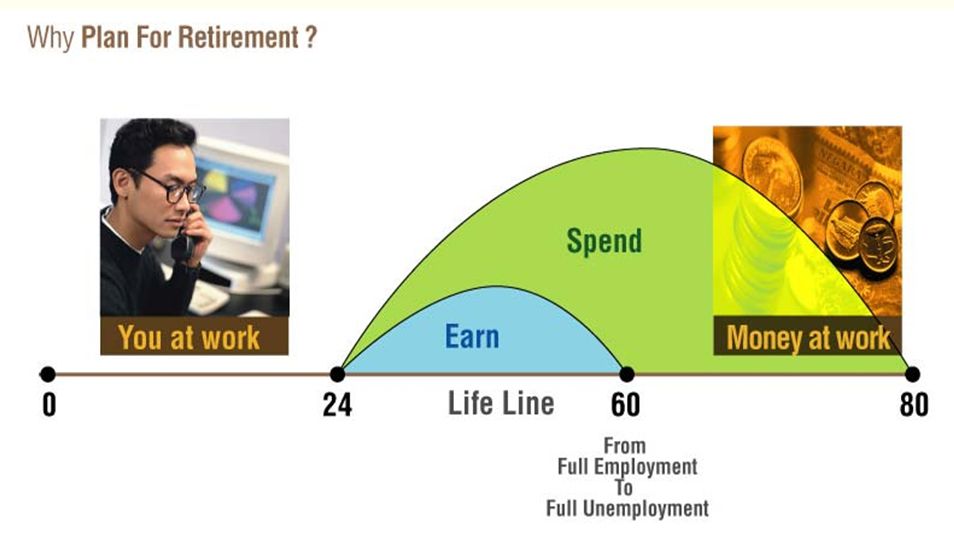

10 Things To Consider Before You Hit Retirement

By Zi Yao Lim . 31 December 2014 https://www.imoney.my/articles/1 ... -you-hit-retirement

You have been working your whole life, saving for your retirement. Most of us have millions of ideas about what it’ll be like when it finally comes to the moment where we break away from the 9-to-5 rut. However, with a few more years to go before the day finally arrives, it’s time to take serious action, and get things in order for your golden years ahead.

Most of us would want to achieve financial freedom by then and having not to worry about money any further. To ensure everything is in order when your last conventional pay cheque comes your way, here are 10 things you need to do:

1. Decide on your goal

Many a times when we plan for our retirement, we don’t have a clear picture of how we really want to retire. Do we want to retire at a small and quiet village, outside of town, or perhaps stay in a small(ish) condominium in town, where everything is within walking distance?

By this time, with just a few years to your retirement, you should really have a clear idea whether you want to upsize or downsize your lifestyle post-employment.

The first question you ought to ask yourself is what you want after you retire. Travel around the world and eventually, retire at one of the Caribbean islands? Whatever your goal is, you need to align your retirement plan towards achieving it.

2. List down your obligations

Before embarking on your adventure after retirement, you should consider any financial obligations you may have that can adversely affect your finances after employment.

Do you still have dependents (parents or children) you have to support even after you retire? Will your child(ren) still be in college, with hefty tuition fees coming your way every few months?

How about your lifestyle? If you have planned for your retirement optimally, you should not have to downsize your lifestyle too much. The key word here is sustainability. You should have a clear idea of how much you need every month during your retirement, and how long your retirement fund will last.

3. Clear your debt

Ideally, you should have cleared all your debts before you hit retirement. By clearing your debts, you improve your net worth and credit rating which might be helpful should you need to take another loan in the future.

Credit card debts are usually the first priority to be cleared off due to its high interest rates, followed by personal loans and car loans. There has been an ongoing debate on whether home loans should be cleared off sooner than needed for the peace of mind of being debt-free. If you think paying off home loan last is a better idea, perhaps you should look into the option of refinancing your mortgage.

Currently, Malaysia’s base lending rate is at 6.85%. Comparing with the historical rates, it might seem to be a little high too high to refinance your mortgage. But consider this: after retirement, you’ll lose your primary source of income (for some, only source of income) and your ability to take up a new loan diminishes.

If you have to refinance your mortgage by then, banks might quote you a higher rate, require a guarantor, or simply reject your application. Perhaps it might be a good idea to lock in a fixed mortgage rate to avoid being exposed to interest rate volatility in times of economic uncertainty.

4. Preserve your assets

When we are still earning an income, we mostly focus on accumulating assets. However, when retirement hits you, more focus should be put on preserving your existing assets.

A person may own multiple properties and be worth millions of Ringgit, but he or she may not be able to even afford lunch! In finance, two terms arise: solvency is the ability to meet its long-term ( more than two years) financial obligations, and liquidity is the ability to meet short-term (less than two years) obligations by converting assets quickly into cash.

In other words, how we preserve our assets depends on our ability to sustain our short-term needs (daily expenses and outflow) without needing to liquidate (force sale) our assets. Consolidating your assets by consulting wealth management and financial planning advisories may be a good idea to have clearer view of your current financial health and have more control in monitoring and preserving your assets.

5. Create or update your will

To prevent your family from exploding into those family feuds infamously depicted in Hong Kong soap operas, updating your will (or create one if you don’t have one yet) is essential. Jokes aside, it is important to have estate planning so that you can be assured that your family is being taken care off in the manner of your preference.

Having a will doesn’t just ensure your hard-earned assets are distributed properly and rightfully, according to your wishes, it also helps your family go through the process quicker and with greater ease. Remember, avoid hassles by having different wills for assets in different countries and jurisdictions.

6. Review your investment portfolio

As you retire, you would require a substantial steady stream of income to replace your previous conventional income that takes care of your daily expenses and other obligations.

As result, your capacity or holding power of your investment is limited. Perhaps toning down your investment appetite from aggressive high capital growth equities to a more conservative and passive, dividend paying funds such as bonds or government securities might be a good idea. Reviewing your risk tolerance is essential to sustain good cash flow and preserve your assets.

Here are some financial mistakes you should avoid before you hit retirement.

7. Establish passive income

If the retirement you envisioned for yourself is one where you stop working completely, it becomes even more crucial for you to establish at least one source of passive income, which will be your new primary source of income.

As an alternative to your investments, you can also create another stream of income by working part-time or taking up freelance jobs. For those who have years of professional work experience, they can opt for consulting or an advisory role to other firms or institutions – this may not exactly be ‘passive’ but if it’s something you enjoy doing, it wont feel like a job for sure!

Setting up a mamak or a sundry shop as a small business might also be a good idea (seriously, mamaks rarely fail and typically have healthy profit margins).

8. Healthcare

The unfortunate thing with healthcare is that it becomes more expensive the older we get. Most people give up one their medical card due to the exorbitant price they have to pay — especially in view of the diminishing income after retirement.

Therefore, it is important for one to have a clear idea of their health and fitness level before they hit their golden years. Prevention is certainly better than cure.

Find out if you have any medical conditions that may require substantial amount of money to finance, especially when healthcare cost is escalating to the tune of 12% per annum. Maintain your medical card, review the policy to ensure it is adequate, then set up a budget for rainy days, that could include medical emergencies.

9. Withdraw your EPF

Should you withdraw everything or should you withdraw a set amount regularly? Prematurely withdrawing and depleting your EPF, even if you can, may bring adverse effect to your retirement savings. Unless you have a strong reason or solid financial plan to invest elsewhere that could potentially provide better returns, EPF should be remained untouched and used as a last resort as this will be retirement fund for the next 10 to 20 years.

If you don’t think your EPF savings enough is adequate to outlive your retirement years, you can consider withdrawing some of the money for selected investments.

10. Continue working

Retirement is really just a phase that everyone goes through. According to the Life After Work survey conducted by HSBC, 22% of Malaysians plan to semi-retire because they need to bridge an income shortfall.

Review your retirement savings before your retirement to have an understanding of whether you stand financially post-employment. Will you be able to live comfortably on that savings, or do you need to continue working to generate income for your golden years?

For some, the idea of not doing anything for next one to two decades may not be conceivable at all! However, the point is to plan for your retirement so semi-retirement is an option and not a means to survive.

We need to start retirement planning as early as possible in order to have a comfortable retirement in years to come. However, planning your retirement is not just about saving money religiously, but also about making the right decisions at the right time to boost your savings.

These 10 steps should be done just a few years before you retire. This will still give you some room to make up for any shortfalls.

To enjoy a comfortable retirement, ensure you have two-third of your pre-retirement income.

(转帖分享)

2015年1月13日星期二

找氣球的启发

50個人走進裝滿氣球的房間後,學到了一件重要的事。

這50個人原本是參加研討會,演講者突然停下並開始小組活動。他做了一個奇怪的要求…

...

他給每個人一個氣球,並請他們在氣球上用麥克筆寫上名字。接著,將這些氣球收集起來,放到另一個房間裡。

.

於是,這些人被帶到那個房間,並被要求找到寫著自己的名字的氣球,限時5分鐘。每個人都瘋狂找尋自己的名字,跟他人碰撞、推擠著,現場一片混亂。

.

5分鐘過去,在場沒有人找到自己的氣球。現在大家被要求隨便找個氣球,然後把氣球遞給上面所寫的名字的人。沒有幾分鐘,大家都得到了自己的氣球。

.

演講者表示,這就是我們的人生。

每個人都在瘋狂尋找快樂,但沒人知道在哪裡。

快樂其實取決於周遭的人:

給他們快樂,你就會得到你的快樂。而這就是活著的意義。

(转帖分享文章)

2015年1月11日星期日

投资者理财建议、执行

投资计划制定,一个完善的投资咨询涉及几个步骤。

1--资料收集,了解投资者投资心态、理念、投资能力、投资目标。

2--理财观念的教育、交流、讨论。

3--分析及设计理财工具(对于基金顾问,则是推荐合适的基金种类)

4--执行、监督及调整投资。

1--资料收集,了解投资者投资心态、理念、投资能力、投资目标。

2--理财观念的教育、交流、讨论。

3--分析及设计理财工具(对于基金顾问,则是推荐合适的基金种类)

4--执行、监督及调整投资。

坚持长远投资目标,不走偏

老牛想在家門與小河邊修一條路,為了讓路筆直,老牛決定先踩出路的輪廓來。

老牛認真地看著腳下,每走一步都要瞻前顧後。幾步後老牛發現,雖然每個步伐都很直,總體卻是歪斜的。

小馬自告奮用來幫忙。牠先向小河眺望了一會兒,然後盯著前方,快速向河邊跑去。小馬的腳印並不十分整齊,但整體是筆直的。

原來,小馬對準前方的目標奔跑,即使腳下稍有淩亂,可方向是一致的,更勝於老牛小心翼翼注意腳下,卻迷失了最終目標。

寓意:投资者只要制定长远目標,努力不懈,不必在意過程中的困難和挫折。反之如果在意眼前利益,患得患失,註定要走偏的。

把眼光放远,投资获取理想回酬的机会大增。

老牛認真地看著腳下,每走一步都要瞻前顧後。幾步後老牛發現,雖然每個步伐都很直,總體卻是歪斜的。

小馬自告奮用來幫忙。牠先向小河眺望了一會兒,然後盯著前方,快速向河邊跑去。小馬的腳印並不十分整齊,但整體是筆直的。

原來,小馬對準前方的目標奔跑,即使腳下稍有淩亂,可方向是一致的,更勝於老牛小心翼翼注意腳下,卻迷失了最終目標。

寓意:投资者只要制定长远目標,努力不懈,不必在意過程中的困難和挫折。反之如果在意眼前利益,患得患失,註定要走偏的。

把眼光放远,投资获取理想回酬的机会大增。

2014年11月29日星期六

2014年11月24日星期一

周杰倫成名之路

15年前的周杰倫,沒錢,沒名,沒女友;而且因為在單親家庭長大,他性格沉默而孤僻,走起路來更是低著頭;他逛街買不起昂貴的,卻也看不上便宜的;家裡唯一的收藏品就是母親買給他的吉他和自己彈斷的一根根琴弦……

周杰倫第一次參加選秀節目,評委批評他唱歌時口齒不清,第一輪就慘遭淘汰。下台之前,坐在評委席的吳宗憲提出要看看參賽選手寫的譜子。唯獨杰倫,連草稿都寫得乾淨而整潔,別的創作型歌手,譜子畫得一團亂麻。看完吳宗憲說:“下週來我公司報導。”因為認真,他得到了人生的第一次機會。那一年,杰倫18歲,他一無所有,只有對音樂的熱愛和一絲不苟的認真。

也許是惺惺相惜吧,杰倫在公司遇上了同樣懷才不遇的填詞人——方文山。然而他們辛苦的付出卻不被認可,他們給當時紅極一時的歌手寫歌,卻沒有一首歌得到保留:

寫過一首名為《眼淚知道》的歌曲,被吳宗憲推薦給劉德華。劉德華只不過輕輕瞟了一眼歌詞,竟連搖頭的說“眼淚怎麼會知道,眼淚要知道什麼呢?”最後給了溫嵐唱;

他們為了向李小龍致敬,給張惠妹寫了一首《雙截棍》,阿妹卻認為曲風怪異,因此不接受;

《可愛女人》寫給吳宗憲,憲哥寫好了詞,叫《春夏秋冬》,可是憲哥實在是唱不來,於是退貨,之後讓徐若瑄填詞;

《忍者》寫給張惠妹,阿妹當時根本無法想像這種稀奇古怪的曲風,更不用說拿來自己唱了,認為不合適被退;

……

一年很快就過去了,依然沒有歌手願意唱他們的歌。

2000年的一天,吳宗憲找到他說:“你這些歌曲,別人不喜歡唱,但是我感覺還不錯,那就你自己來唱,如果你三天之內能寫出個十幾首歌,我就從中挑出十首歌,給你出一張專輯。”

杰倫深知這也許是自己唯一的機會了。他先去買了一整箱的泡麵,然後把自己關進工作室了,那次真的完全拼了命,居然寫歌寫到流鼻血……

十天之後,同名專輯《Jay》橫空出世,當年在台灣拿下五十萬張的銷量。杰倫紅了,杰倫的名字,傳遍台灣,吹到大陸,後來當電影導演也是水到渠成的事,他和方文山也成了絕配的搭檔。

周杰倫不容易,也知道自己的長短,自知自己不是“讀書的料兒”,他從不花費時間去做跟音樂無關的事。

一個男生,可以不帥,可以不唸書,可以沒錢,可以不善言談,但是一定要對自己所鍾愛的事業認真!否則,你的一生也就這樣了。

正如杰倫所說:一個厲害的人、不平凡的人,書不一定要讀得多好,但是一定要有一技之長。

(转帖分享)

订阅:

博文 (Atom)